|

Law & Ethics Update |

|

Failure to Maintain Complaint-Handling Procedures §626.9541(j)

Misrepresentation in Insurance Applications §626.9541(k)

· Knowingly making a false or fraudulent written or oral statement, representation on, or relative to, an application or negotiation for an insurance policy for the purpose of obtaining a fee, commission, money, or other benefit from any insurer, agent, broker, or individual. · Knowingly making a material omission in the comparison of a life, health, or Medicare supplement insurance replacement policy with the policy it replaces, for the purpose of obtaining a fee, commission, money, or other benefit from an insurer, agent, broker, or individual.

Free Insurance Prohibited §626.9541(n)

Illegal Dealings in Premiums; Excess or Reduced Charges for Insurance §626.9541(o)

· Once a premium payment reaches your hands, you need to submit it on behalf of the client, immediately and in the manner it was paid. · Don’t impose or request an additional premium for a policy of motor vehicle liability, personal injury protection, medical payment, collision insurance or any combination of these. You cannot refuse to renew a policy solely because the insured was involved in a motor vehicle accident, unless the insurer’s file contains information from which the insurer, in good faith, determines the insured was substantially at fault in an accident. · Anyone otherwise qualified can be a director of two or more domestic competing insurers, unless the effect is to lessen competition to generally or materially create a monopoly. · This does not apply to those who are directors of two or more insurers under common control or management.

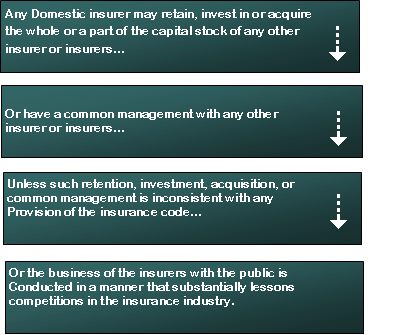

Interlocking Ownership and Management §626.9541(r)

Prohibited Arrangements as to Funerals §626.9541(s)

· A life insurer cannot designate who will conduct an insured’s funeral. The insurer cannot organize, promote, or operate any enterprise, or plan to enter into any contract, with any insured, under which the freedom of choice in the open market of the person is restricted as to the purchase, arrangement, and conduct of a funeral service for any insured by the insurer.An insurer cannot contract or agree to furnish funeral merchandise or services in connection with the disposition of an insured at death. · An insurer cannot contract or agree with any funeral director (or direct disposer) promising a funeral director consent to conduct the funerals of insureds of the insurer. · An insurer will provide, in any insurance contract covering the life of a Florida resident, for the payment of proceeds or benefits in U.S. dollars. The insured will not withhold proceeds or benefits for the purpose of providing, inducing, or furthering an arrangement or agreement designed to require the employment of a particular person to conduct the funeral.

Inpatient Facility Network §626.9541(3)

Participation in a Wellness or Health Improvement Program §626.9541(4)

Favored Agent or Insurer; Coercion of Debtors §626.9551

· Require, as a condition precedent or subsequent to the lending of money or extension of credit or renewal, that the person to whom money or credit is extended, or whose obligation the creditor is to finance, negotiate any policy or contract of insurance through a particular insurer, group of insurers, agent, broker, or group of agents or brokers. · Reject an insurance policy solely because the policy has been issued or underwritten by a person not associated with a financial institution, subsidiary or affiliate, when the insurance is required in connection with a loan or extension of credit; or unreasonably disapprove the insurance policy provided by a borrower for the protection of the property securing the credit or lien. This disapproval is deemed unreasonable if it is not based solely on uniformly applies reasonable standards, relating to the extent of coverage required by the lender extending credit and the financial soundness and services of an insurer. Standards cannot discriminate against any particular type of insurer, nor can standards call for the disapproval of an insurance policy because the policy contains coverage in addition to that required. · Require any borrower, mortgagor, purchaser, insurer, broker, or agent to pay a separate charge in connection with the handling of an insurance policy required in connection with a loan or other extension of credit, or pay a separate charge to substitute the insurance policy of one insurer for another, unless the charge would be required if the person were providing the insurance. · Provide to others or use insurance information required to be disclosed by a customer to a financial institution, subsidiary or affiliate, in connection with the extension of credit for the purpose of soliciting the sale of insurance, unless the customer has given express written consent or the opportunity to object to use of the information. Insurance information means information concerning premiums, terms, and conditions of insurance coverage, insurance claims, and insurance history provided by a customer. The opportunity to object to the use of insurance information must be in writing and clearly and conspicuously made.

· Federally or state-insured depository institutions and credit unions must make clear and conspicuous written disclosure prior to the sale of any insurance policy that policies ARE NOT deposits, are not insured by the FDIC or any other entity, are not guaranteed by the insured depository institution or any person soliciting the purchase or selling the policy; that the financial institution is not obligated to provide benefits under the insurance contract; and, where appropriate, that the policy involves investment risk, including potential loss of principal. · All documents constituting policies of insurance must be separate and cannot be combined with or part of, other documents. A person may not include the expense of insurance premiums in a primary credit transaction without the express written consent of the customer. A loan officer of a financial institution involved in the application, solicitation, or closing of a loan transaction cannot solicit or sell insurance in connection with the loan, but may refer the customer to an insurance agent who is not involved in the application, solicitation, or closing of the same loan transaction.

Power of Department and Office §626.9561

The department and office each have power, within their respective regulatory jurisdictions, to examine and investigate the affairs of every person involved in the business of insurance in order to determine whether any person has been or is engaged in any unfair method of competition or in any unfair or deceptive act or practice and each has the powers and duties specified in Defined Practices; Hearings, Witnesses, Appearances, Production of Books and Service of Process.

Defined Practices; Hearings, Witnesses, Appearances, Production of Books and Service of Process §626.9571 Whenever the department or office has reason to believe a person in Florida has engaged, or is engaging, in an unfair method of competition, unfair or deceptive act, practice, or is engaging in the business of insurance without being properly licensed as required, and that a proceeding would be in the best interest of the public, it will conduct a hearing in accordance with the Administrative Procedures Act.

· Suspension of any license or authority of any rating organization or insurer that fails to comply with an order of the office within the time stated by the order, or extension of the order. · The office cannot suspend the license or authority of any rating organization or insurer for failure to comply with an order until the time prescribed for an appeal has expired, or, · If an appeal has been taken, until the order has been affirmed. · The office may determine when a suspension of license or authority will become effective and it will remain in effect for the period fixed by it, unless it modifies or rescinds the suspension, or until the order, upon which the suspension is based, is modified, rescinded, or reversed.

Life or Disability Insurance; Illegal Dealings §626.9705

· Establish or charge a premium or rate to an applicant or a prospective policyholder, or · Establish or charge an unfair, discriminatory premium or rate to such person à Based solely on the grounds that the applicant or policyholder suffers from a severe disability.

Severe Disability means: · A spinal cord disease or injury resulting in permanent and total disability · Amputation of any extremity that requires prosthesis · Permanent visual acuity of 20/200 or worse in the better eye with the best correction à A peripheral field that the widest diameter of the field subtends an angular distance no greater than 20 degrees, or · Neurosensory deafness Nothing should be construed as requiring an insurer to provide insurance coverage against a severe disability that the applicant or policyholder has already sustained.

Life Insurance; Discrimination on Basis of Sickle-Cell Trait Prohibited §626.9706

No life insurance policy issued and delivered in Florida can carry a higher premium rate or charge solely because the person to be insured has the sickle-cell trait. [See also §626.9707, Disability Insurance; Discrimination of Basis of Sickle-Cell Trait Prohibited]

Life Insurance Solicitation §626.99

· Information that will improve the buyer’s ability to select the most appropriate plan of life insurance · Improve the buyer’s understanding of the basic features of the policy purchased or under consideration · Improve the ability of the buyer to evaluate the relative costs of similar plans of life insurance

Statute does not prohibit an insurer from using additional material, if not a violation of any statute or regulation.

© 2024 Wall Street Instructors Online LLC No part of this material may be reproduced without the written permission of the publisher. |